On Life:

The biggest personal update is that I founded an organization, called Kingdom Wealth Building. Last year I was able to present the content 5 times to three church communities in three U.S. states. Aside from Peloton, all of my sweat now goes into this project. I spent the holiday season remodeling the website, so take a peek at KingdomWB.org and please share with others as God may nudge you. Feedback is always welcome!

On the Market:

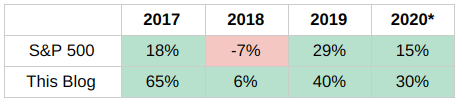

There are many ways to define “the stock market,” but by any measure 2022 was one of the worst years in its history. Back in October, I attended an event where a speaker noted that 2022 was one of the 7 worst years ever, with the other 6 occurring during The Great Depression. And then after that things got worse, with the market declining 20% by the time December 31 arrived.

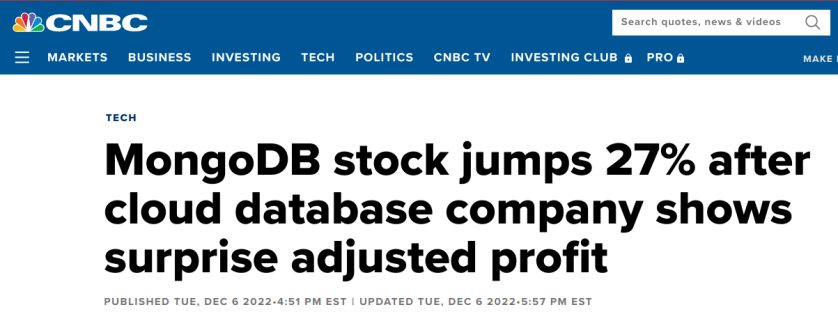

But wait, there’s more! The picks I recommended last year did even worse than the downtrodden market, as MongoDB declined 60%, Unity declined 79%, and the talk of “Web3” was probably the most badly-timed thing I’ve uttered since the day I congratulated a coworker on being pregnant (she was not). Therefore I’ll understand if some of you decide to stop scrolling. For the rest, here’s an overly simplified take on what happened:

When the Music Stops

Many factors caused the stock market to suffer mightily in 2022, but the most important is that the government changed its approach to the money supply. For over a decade, the gov had consistently printed lots of extra money. Boosted by relatively loose lending policies, the money flowed through all areas of society, enabling businesses and individuals to spend with relative ease. This progressively increased the prices of pretty much anything considered an asset — from stocks to houses to baseball cards — and yes of course, crypto.

Eventually the rising prices became noticeably measurable as inflation, and the government has been trying to remove money from the system — rapidly — ever since. This process is healthy for markets in the long run, but ideally it happens more gradually, enabling businesses to adjust without having to do things like layoffs. Unfortunately trying to remove money this quickly, especially after years of so much indulgence, is a recipe for a stock market crash.

Babies in Bathwater

Conditions like these are tough for almost everyone, but technology companies and future-oriented “growth stocks” tend to be particularly vulnerable to such changes in money policy. Once it became clear the government had truly found religion, Wall Street slashed the prices of companies in that category severely. It didn’t seem to matter that some companies were of better quality than others, they pretty much all got cut in half (or more)

Throughout 2022 there were periods when stocks in that category were all down by exactly the same percentage. This despite the fact that they differed substantially in terms of margins, debt, and competitive positioning. Wall Street is supposed to evaluate these and other criteria to determine a reasonable stock price. Each time I observed such evidence of herd-mentality thinking, it suggested that Wall St. was applying a broad brush to all companies in the space, meaning there would be ample opportunity for the truly quality ones to surprise:

Two Baskets

As 2023 begins there are massive global uncertainties, such as the Russia-Ukraine war, recent changes in China’s response to covid, and governments that hope to curtail inflation by causing layoffs, just to name a few. One thing that seems to be consensus is that there will be some type of recession in the first half of the year. Given all that, I’m taking a two-pronged approach to buying stocks in 2023.

The first basket of stocks I’m recommending is simply about surviving the year 2023. These picks are: Dollar General (DG), Walmart (WMT) and Dollar Tree (DLTR). It’s a relatively conventional strategy — during recessions consumers become more thrifty, bypassing their usual stores in favor of passable goods from low-cost providers. It’s also a crowded trade already, as these three firms widely outperformed the S&P 500 in 2022. However, the point of this strategy is just to survive. If this trade doesn’t work, that will likely have meant the economy did much better in 2023 than the bad scenarios that seem quite plausible today, in which case mostly everyone will be better off in many ways, including financially. Lastly remember that wherever people end up going for their needs, Visa (V) and Mastercard (MA) will benefit, so I recommend both as safe havens for this coming year as well.

The other basket is about buying stocks to thrive beyond the year 2023. The tough economic landscape of today provides a promising buying opportunity for the next decade. In this basket I’m placing only one stock, Cloudflare (NET). Like MongoDB in the example above, I anticipate that Cloudflare’s stock price may suffer in the near term (in line with its sector) but I also expect it to positively surprise Wall St. many times over. There are other “baby in the bathwater” stocks I would love to write about here, but I’m being more cautious after the disaster that was 2022.

Cloudflare is a company I have high conviction about in terms of business model and long-term competitive advantage. Unlike flashy “tech stocks” that simply rode the wave of hype during the last cycle, Cloudflare has spent years building massive infrastructure across the globe. They can increasingly leverage their buildout for profit, at a rate I don’t think Wall Street will expect. Although 2023 may be yet another bumpy ride, those who are able to buy Cloudflare periodically — especially during market selloffs — should feel very good about that choice a half decade from now.

Final Thoughts on 2023

There are very sobering realities that suggest 2023 will be another rough year for the stock market. I don’t wish to minimize those. Looking back at 100 years of history, it’s rare for the market to decline in two consecutive years, especially after a double-digit fall like we saw in 2022. Unfortunately, the last time that did happen was during a stretch of 2000-2002, and there are many aspects of this recent cycle that seem to closely mirror what happened in that era.

However it also seems quite plausible that by the end of 2023 things will be looking up, especially because stocks are forward-looking by their nature. This moment is either one of the toughest times to invest or one of the absolute best in recent memory; it all depends on your timeline and psychology. Either way, I wish you well and hope to see you next year.

— Jan. 4, 2023